Cross-Border Payments With Blockchain – Are They Truly Faster And More Affordable?

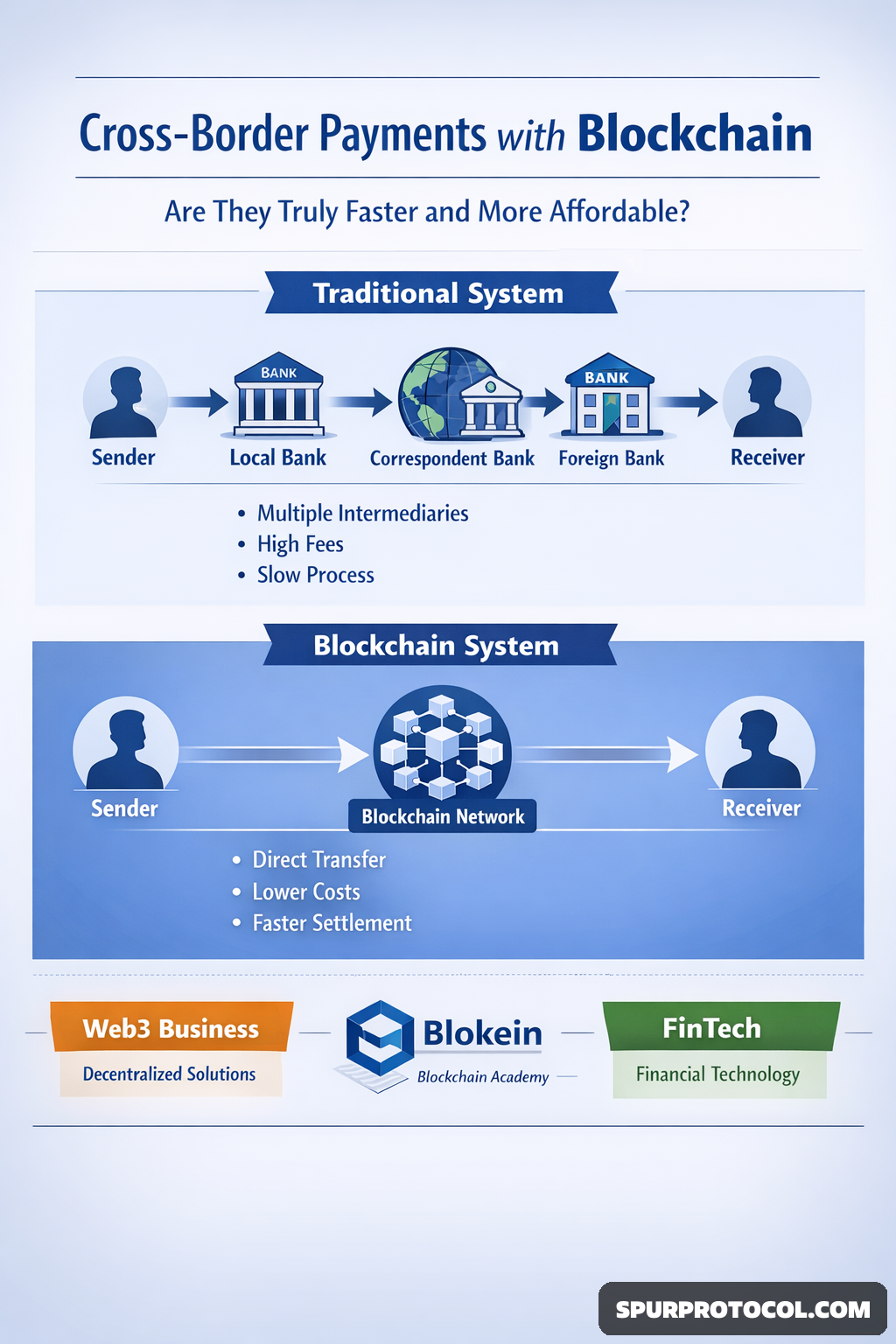

International money transfers have long been associated with delays, high fees, and operational complexity. In the traditional system, funds typically pass through multiple banks, involve currency exchanges, and move across various clearing networks before reaching the final recipient. Blockchain technology proposes a more streamlined alternative. The key question, however, is whether it genuinely delivers faster and cheaper cross-border transactions.

Go Back

🕒 2:14 PM

📅 Feb 23, 2026

✍️ By Goko7

How the Traditional System Operates

Conventional cross-border payments rely on correspondent banking relationships. When money is sent internationally, it often travels through several intermediary banks before settlement. Each institution involved processes the transaction and applies its own fees, which increases the total cost and extends the processing time.

Settlement may take several business days, particularly when transactions span different jurisdictions, time zones, or regulatory frameworks. Currency conversion margins and compliance procedures—such as anti-money laundering (AML) and know-your-customer (KYC) checks—can further raise costs and slow down the process. For businesses and individuals alike, these factors can reduce efficiency and profitability.

The Potential Benefits of Blockchain

Blockchain-based payment systems function on decentralized networks that enable peer-to-peer value transfer. By reducing or eliminating intermediaries, these systems can simplify transaction flows and lower certain operational expenses.

One of the most significant advantages is speed. Many blockchain networks can confirm transactions within minutes rather than days. Additionally, blockchain operates continuously—24 hours a day, seven days a week—without being restricted by banking hours or holidays. This constant availability can be particularly beneficial for global trade and digital commerce.

Hidden Costs and Practical Limitations

Despite its advantages, blockchain does not automatically guarantee lower costs in every scenario. Network transaction fees can fluctuate depending on demand and congestion. Moreover, converting digital assets into local fiat currencies may introduce additional expenses through exchange platforms or liquidity providers.

Regulatory compliance, integration with legacy financial systems, and local legal requirements also influence the overall efficiency of blockchain-based transfers. Another consideration is cryptocurrency price volatility, which can create financial risk unless stable digital assets are used.

A Strong Alternative, Not a Full Replacement

Blockchain has demonstrated clear potential to accelerate international payments and reduce certain fees. However, it does not remove all financial, operational, or regulatory complexities. At the same time, traditional financial institutions are investing in technological upgrades to improve their own cross-border services.

In practice, blockchain-powered cross-border payments can be faster and, in specific use cases, more cost-effective. As infrastructure matures and regulatory clarity improves, blockchain solutions are likely to become an increasingly important component of the global payments ecosystem—though not necessarily a complete substitute for existing systems.