How To Start Mining Cryptocurrency

How to Start Mining Cryptocurrency

Go Back

🕒 4:17 PM

📅 Jan 26, 2025

✍️ By Mecuzy

How to Start Mining Cryptocurrency

Go Back

🕒 4:17 PM

📅 Jan 26, 2025

✍️ By Mecuzy

Mining is the process by which new cryptocurrency tokens or coins are generated. It bears little resemblance to the work done by those who physically mine for precious metals like gold—the necessary tools are an internet connection, compatible devices, and the correct software. However, the comparison does hold; virtual currency miners use computers to solve cryptographic problems and receive a reward in the form of cryptocurrency.

Learn how to get started mining your favorite cryptocurrency and how to determine the costs you'll incur to do so.

In cryptocurrency lingo, mining is the term for work done to open a new block on certain blockchains. The first miner to solve the cryptographic puzzle receives a cryptocurrency reward.

With that in mind, one of the first steps to take if you're interested in being a cryptocurrency miner is to learn which cryptocurrencies can be mined. Bitcoin (BTC), Monero (XMR), and Litecoin (LTC) are examples of coins that can be mined.

The most profitable cryptocurrencies have become much more difficult to mine than in the past. Most have a mining difficulty that increases over time, and the number of miners with large-scale mining operations has taken over most of the hashing power of each cryptocurrency's network. Hashing power is how many calculations per second a network can complete.

Not every cryptocurrency can be mined because not all use a competitive reward system.

Some cryptocurrencies require expensive hardware to mine, and overwhelming demand for this equipment has caused the cost and effort associated with setting up a rig to skyrocket. Others may be more accessible in terms of the equipment that you need. The costs alone make it worthwhile to take the time to plan how and what you'll mine.

There are generally three basic components to a mining operation: the wallet, the mining software, and the mining hardware.

You'll need a wallet for your cryptocurrency to store the keys for any tokens or coins your mining efforts yield. Wallets have a unique address, allowing you to send and receive tokens securely. There are many types of wallets, and it's best to use a "cold storage" wallet to store your keys offline for security. Decide which one is best for your needs before you start mining.

Most mining software is free to download and use and is also available for various operating systems. For popular cryptocurrencies like Bitcoin, you'll find that multiple types of software can be used. While many of these options will be effective, slight differences could impact your mining operation.

Mining Hardware

Mining hardware may be the most expensive component of a mining rig setup. You'll need a powerful computer, perhaps even one specifically designed for mining, like an ASIC miner.

An ASIC miner is a pre-built mining rig; these can be very expensive. For example, the Bitmain Bitcoin Miner S19 XP costs about $4,600.1 The S19 XP has a hash rate of 141 terahashes per second (TH/s). You can purchase higher-performing miners, but the price goes up significantly. The Bitcoin Miner S21 mines at 200TH/s and costs about $7,000.2 From that point, miners are more than $10,000, with the Bitcoin Miner S21 Hyd. going for more than $11,000—but it has a hash rate of 335 TH/s.3

There are mining rigs designed for other cryptocurrencies, so you'll need to search for ones compatible with the algorithm used by the cryptocurrency you've chosen. The Bitmain website lists their different products and the algorithms they are compatible with. Some of the mining algorithms are:

Bitmain isn't the only ASIC manufacturer to choose from. There are several others:

It is possible to build a mining rig. The higher the hashrate, the more profitable mining can be—but the more you'll pay.

Home Computers

You can build a computer capable of mining some cryptocurrencies, but you'll need specific hardware. Most graphics cards from Nvidia are capable of mining. However, most are not fast enough to be worth buying for mining purposes.

As of Oct. 6, 2024, the RTX 4090 is the top-of-the-line consumer graphics card. It costs about $1,700 and, depending on the mining algorithm, can hash about between 250 mega hashes per second (MH/s) and 12.7 GH/s—significantly less than one of the Bitcoin ASIC miners.4

It is possible to build multi-GPU mining rigs, but it can still take years to recoup your expenses and begin making a profit. Keep in mind that you may still be unable to mine crypto profitably on your own with a multi-GPU rig—a multi-GPU rig with four RTX 4090s would net you about $3.89 per day mining for the pool NiceHash (after accounting for electricity). In October 2024, RTX 4090s were not being restocked in anticipation of the next generation of cards, so prices were rising. Your costs would be about $8,000 for just the four graphics cards, and it would take about 5.6 years to recoup the expense if net income from mining remained the same.5

You'll also need to purchase the additional hardware to build the computer, such as a power supply, motherboard, processor, memory, and drives. This might cost you several thousand dollars, depending on your chosen setup. Your graphics cards will likely also wear out after several years of 24-hour mining and require replacing, adding to your costs.

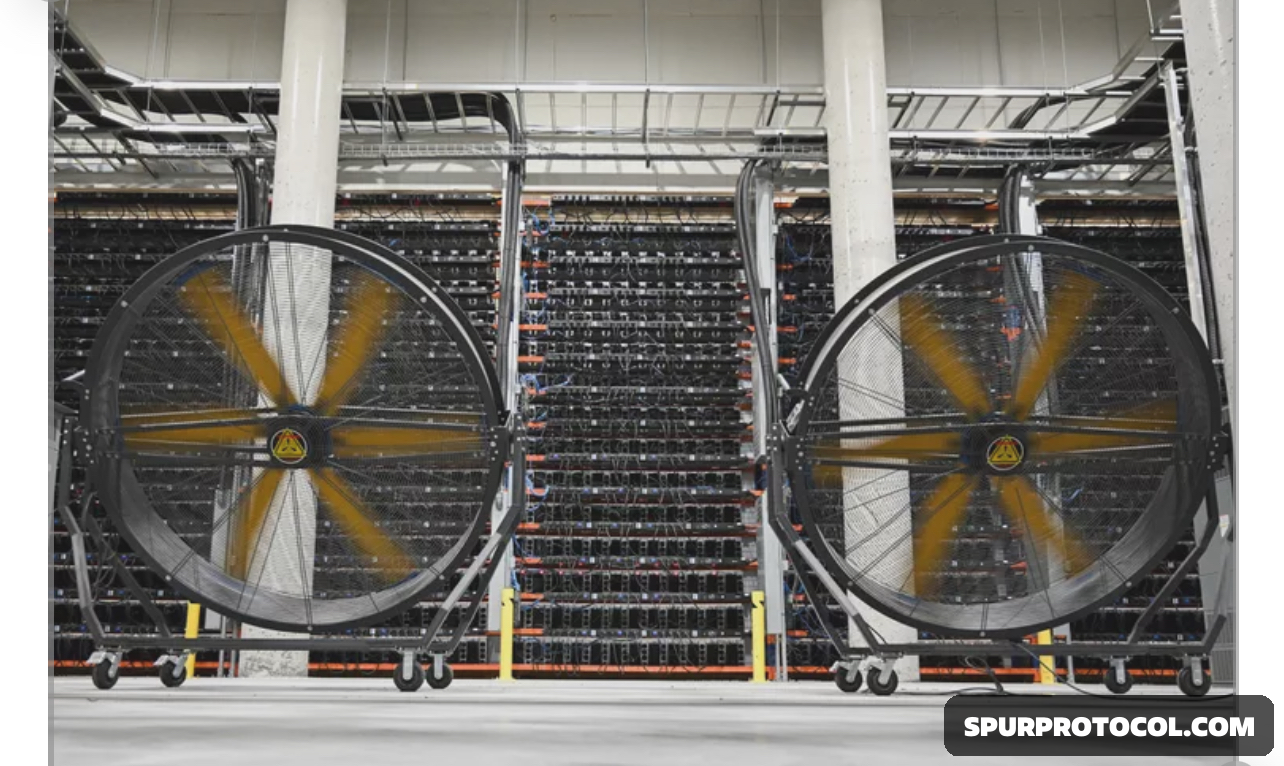

It's important to note that one mining rig, even the S21 XP Hyd., cannot outmine the mining farms and pools. For example, on Oct. 6, 2024, the mining pool FoundryUSA accounted for roughly 29% of the Bitcoin network's hash rate, about 197 EH/s—197 million TH/s.6 You'd need more than 907,500 S21 XPs to keep up with this pool (a cost of over $6.4 billion).

Essentially, a mining pool is a group of miners who combine their computing power and work together to mine. They share the profits proportionally to the amount of work each worker was able to contribute to the process. As you might expect, mining pools offer advantages and disadvantages.

On the one hand, the cost and effort associated with the initial setup are much lower than if you were buying an ASIC or building a multi-GPU mining rig. On the other hand, you're likely to earn much less money from the process, as you'll split any mining rewards with a large group.

Weigh the Return on Investment

The process of mining remains an exciting and potentially profitable one. However, there are several pitfalls. For example, many miners have spent a lot of money setting up their rigs, only to find they cannot recoup the costs with their mining efforts. Ensuring you are armed with as much of an understanding of the mining process and expenses as possible will help protect against this possibility.

There are websites created that can give you estimates of how much you'll be able to generate using specific hardware. The operators of the mining pool, NiceHash, have put together an informative webpage that allows you to input your mining hardware and receive return estimates based on the equipment of users in their pool. This tool can help you determine whether you'll generate enough from your hardware to pay for it, continue earning, and how long it will take.

It depends on many factors. On average, it takes 10 minutes for the network to create a new block and the miner(s) to receive the reward of 3.125 BTC.7The reward is split according to pool payout rules. With pools splitting rewards, it can take a significant amount of time to earn one full cryptocurrency. One person mining 0.000065 BTC (four RTX 4090s on Oct. 6, 2024, using NiceHash) per day would take more than 42 years (about 15,384 days) to earn 1 BTC, all else, such as block rewards, hash rates, and pool payouts, remaining the same.

Is Cryptocurrency Mining Illegal?

Cryptocurrency is legal in most countries and illegal in some, but regulations are still developing worldwide. Many countries are cracking down on the practice by imposing hefty taxes or other measures that discourage mining rather than announcing outright bans.

Mining crypto is very competitive due to cryptocurrency's values. It was possible in the early days of crypto to mine several coins per year, but mining difficulty and competitiveness have increased so much that it is profitable only for those who can afford large-scale mining operations. However, making between $10 and $100 monthly mining cryptocurrency is still possible with the proper equipment.

Cryptocurrency mining is discovering the solution to a cryptographic problem and receiving a reward of cryptocurrency. It can be very expensive to set up a miner capable of competing with the rest of the network you've chosen, so it's best to join a mining pool and share the work and rewards with others.